Ownless

OWNLESS

Read along as I spiral into American history starting with the question “Is now a good time to buy a house?”

As a 30 year old who (like most I assume) has recently begun freaking out about his financial future — and as one who hasn’t necessarily achieved financial goals, such as being able to afford a house— I have a lot of doubts. Nevertheless I’m nearing that point, so I took to the internet to learn as much as I could about Buying A House… starting with the big question —

Chat, Given the macro trends as of may 2026… for someone looking to buy a home in America, how does the timing look? is it good time to buy or wait to see how things shake out?

—

I read up on Fannie Mae and Freddie Mac; first of all what the dystopian fuck? I’m not going into it for this piece, but that Fannie and Freddie consistently rank in our top 5 (currently 1 and 3) corporations with over 4trillion in assets a piece ? Or how many people even know that banks sell your loans within days to Fannie and Freddie, back into your neighbors 401k ? The names themselves are the dystopian kicker for me, but moving on.

I got to know RATES a bit better…

Ive long understood that RATES hang over the housing market like a sorting hat. It’s a constant talking point on financial news and I’ve been a real-time follower through Chairmen Powell’s tenure.

Still I had no idea how Rates would matter to me as a home-buyer, so I had two questions:

First, why the rate number matters so much?

The rate percentage becomes a monthly payment multiplier, so the difference between 5% and 7% on a $400,000 loan is about $500/month swing. Over 30 years, that rate difference costs you more than the house itself did.

|

Rate |

Monthly P&I |

Total paid over 30 yrs |

Interest paid |

|

5.0% |

$2,147 |

$773,000 |

$373,000 |

|

6.0% |

$2,398 |

$863,000 |

$463,000 |

|

6.5% |

$2,528 |

$910,000 |

$510,000 |

|

7.0% |

$2,661 |

$958,000 |

$558,000 |

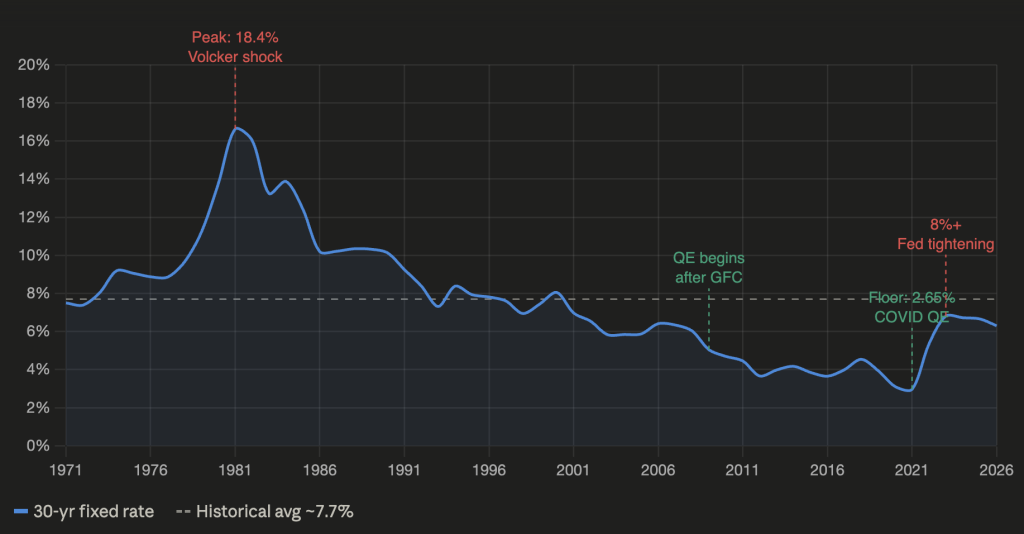

Second, are rates a natural phenomena that react to a market, or can they be purposefully set? I wanted to know the history of the number — am I waiting around for a miracle or can someone at the FED up and decide its time we return to 2 percent?

I learned that rates are policy instrument, not a natural phenomena and they began in 1971 at around 8%. They peaked in ’81 with the VOLCKER shock (more on that in a moment) and hit a floor during COVID ’21 with 2.65% rates (!!) — How are those homeowners doing today? —

Now the historical avg. sits at roughly 7.7% but that seems skewed by the Vocker shock. So what was it? Without going all the way into monetary policy, let’s say from a historical fans view, this was the most dramatic rate event in modern history; the then-FED chair Paul Volcker said fuck it and brought on a brutal recession that successfully killed inflation in about 18 months time.

The fallout, however, was real. And this is where my research took a FREAKONOMICS turn…

Buying a home at 18% meant the interest alone on a $100k loan was $18,000/year. Most people couldn’t. They say unemployment peaked at 10.8% in 1982, inflation dropped to ~3% and by the mid 80’s we set up a 20-year expansion period… Maybe Paul Volcker engineered a concentrated, short-term destruction to break a structural feedback loop that would have compounded indefinitely. But at what cost?

The data says 10.8%, but how much of America went under with that percent? These people have families, and no doubt the cultural zeitgeist would have something to show of it. You don’t force your working class into poverty without some socio-cultural consequences.

Including workers who had stopped looking and underemployed workers who couldn’t find steady full-time work, the real unemployment figure was closer to 20%. And a huge majority (possibly 90%) of job losses hit mining, construction, and manufacturing. Those are household-provider industries, meaning one job loss cascades into a spouse pulling kids from activities, a parent moving in, a small business losing its customer base. The multiplier on that original 10.8% official unemployment into actual household disruption is probably 3–4x and we’re just getting started. What about the psychological toll?

Decades of success turned into failure overnight seemingly; an invisible American collapse in the farm crisis as well as the emergence of modern homelessness can be traced directly to the Volcker shock. By 1990, the confluence of high unemployment, deep cuts to HUD (from $29 billion in 1976 to $17 billion by 1990), deinstitutionalization of the mentally ill, and the emergence of HIV/AIDS created a new structural class of homeless Americans. *Before this moment, homelessness was largely a transient/skid row phenomenon— men between jobs, seasonal workers. After 1982, homelessness became chronic and structural.

I know what you’re thinking— how about the crack cocaine?

And you’re right, the timing is not coincidental. Powder cocaine was an expensive 1970s professional class drug.

Crack, a smokable, cheap, far more addictive, appeared in inner cities in the early-to-mid 1980s, spreading rapidly through neighborhoods already gutted by unemployment. Young men with no manufacturing jobs to enter saw dealing as the only available economic ladder

Sounds a bit like widely available drugs of today: streaming, social media, algorithms, endless scrolls.

It’s possible to say that The Volcker shock is the origin event of modern American inequality structure.Before it: unionized manufacturing provided a genuine middle-class floor for people without college degrees. After it: those jobs didn’t come back. Volcker might have ‘fixed’ the monetary system, but the human cost has compounded for 40 years; here we are.

How we doing?

More specifically, is there a parallel thats in the technological transition and the way its creating new classes / new Homeless/Listless structurally?

At the heart of this question is the assumption that Volcker Shock destroyed a class formation mechanism — the pathway by which people without college degrees could enter a dignified economic middle through physical mastery and unionized labor. The service economy that followed and dominates today was non-union, lower wage, and offered no accumulation logic — you could work at McDonald’s for 30 years and have nothing to show for it structurally.

Post-Volcker America produced a bifurcated class structure: knowledge workers on one side, service workers on the other, with manufacturing’s middle hollowed out. AI is now bifurcating within the knowledge worker class:

At the top: the infrastructure owners — NVIDIA, Anthropic, the hyperscalers — compounding capital at rates with no historical precedent outside Standard Oil. Alongside them, the augmentation class: the lawyer who bills for ten, the solo developer shipping what used to require a team, the consultant synthesizing two hundred documents before lunch. These people are doing extraordinarily well because their leverage is expanding and the tools are working for them.

Below that line, not so much. You find workers whose specific output is now producible at near-zero marginal cost. The work of a junior paralegal, a staff writer, a mid-level analyst or an entry-level coder is still needed but the willingness to pay a human to produce it is collapsing.

And that means the price of the skill is being driven toward zero, which is the rust belt equivalent, and the people in it are being told the same thing the steelworker was told in 1983: just adapt. Technically true at the individual margin, but structurally useless at population scale.

Another trillion-dollar deal gets announced as college graduates get laid off.

The steelworker knew what he lost.

The replacement (AI output) is indistinguishable in form from their output, which means there’s no clean “the machine can’t do what I do” defense. The steelworker could say the robot welded worse. The junior analyst cannot easily say the model synthesizes worse… The surrounding rhetoric tells them the tool is their fault — “just learn to use AI,” “prompt engineering is a skill,” “you need to adapt.” This is the structural equivalent of telling the steelworker in 1983 to “just learn to code” — technically true at the individual level, structurally useless at the population level.Their identity was built on being smart — on cognitive capability as the core self-concept. AI attacks the identity directly, not just the income. The steelworker’s dignity was in physical mastery, community, and production. The knowledge worker’s dignity was in being the person who could think through the problem. When the thinking gets commoditized, the identity dissolves in a way that doesn’t have a clear external target.

So what fills the vacuum?

let’s run down some of the downstream cultures —

Vacuum fillers…

Content creation economy. The influencer/creator economy has the exact same tournament structure as the drug economy Levitt described— a tiny number of people at the top capturing enormous value, a vast base doing the work for near-zero return, sustained by the lottery logic that you might be the one who breaks through. Most won’t—

Crypto and trading. Same tournament structure. Accessible, has the aesthetics of merit (you did the research, you made the call), produces occasional spectacular winners who become visible proof of concept. Functions as a substitute economic identity for people who lost their professional one.

Gig labor. Same race-to-bottom as post-industrial service work. Uber, TaskRabbit, freelance platforms — structurally equivalent to the McDonald’s floor that replaced the factory floor. Accessible, no accumulation logic, no union, no path.

The attention economy itself as both product and trap. The listless knowledge worker consumes more — more content, more distraction, more stimulation— because the cognitive energy that used to go into meaningful work has nowhere to route. The platforms profit from the vacancy.

And why do they turn to the Crack to begin with? Why not when elsewhere there’s no on-ramps?

… The Volcker shock destroyed the manufacturing floor and nothing replaced it for the working class. The damage compounded for 40 years until now AI begins destroying the knowledge work floor— those entry-level, junior, trainee tiers that taught people the craft through repetition and exposure before they became the senior person who could actually do the judgment work. If you eliminate that backbone, you also eliminate the training pipeline for the senior lawyer, the partner, the editor. The craft transmission breaks, leaving one hell of a displaced worker.

Let’s conclude with a final take —

What if the new class is ‘ownless’ — as in they don’t have their own thing, and they don’t own their things?

Ownless is about relation to the world — a structural condition that’s simultaneously economic, psychological, and existential.

Not owning your home?

no equity, no accumulation, no stake in a place.

Not owning your tools?

platform dependency (Adobe, Spotify, AWS, the app store)

Not owning your content?

TikTok, Instagram, Substack can deplatform you

Not owning your skills’ value?

The company owns the IP, AI commoditizes the output

Not owning your attention?

subscriptions, algorithmic feeds, rent-seeking on cognition

Not having your own thing?

no project, no craft, no enterprise that is yours

The pattern has a problem: every relationship to value has been converted from ownership to access, and access is revocable.

If access is in the hands of very few, how do we know we can trust them? We know they’ve destroyed our every accumulation mechanism and replaced it simulation: the level-up, the follower count, the streak: these are progress-shaped experiences with no structural stake underneath. The drive to build something gets routed into systems designed to absorb it without producing anything that is actually yours.

The subscription economy, the gig economy, the rental market, the SaaS model, the streaming model — these are all ownership-to-access conversions that are enormously profitable precisely because they eliminate the customer’s ability to accumulate. A mortgage builds equity. A rent payment builds nothing. That’s not a bug for the landlord — that’s the entire model.

Adobe’s shift from perpetual license to Creative Cloud subscription: the software didn’t change. The ownership relation changed. The user went from owning a tool to renting access to a tool. Adobe’s revenue became predictable and compounding. The user lost the ability to say “I own Photoshop” and gained a permanent monthly obligation with no exit that doesn’t cost them the tool entirely.

Spotify: musicians went from selling records (ownable objects, accumulation artifacts, cultural property) to streaming (access events, fractions of cents, platform dependency). The listener went from owning albums to renting a catalog. Both sides of the transaction were converted from ownership to access. Spotify captured the accumulation.

This is the underlying architecture: the ownless condition is the consumer-side experience of someone else’s accumulation model. Every time ownership is converted to access for the user, it’s converted to recurring revenue for the platform. The ownlessness is the product.

The ownless person never had the thing to begin with, which means the psychological experience isn’t loss — it’s something closer to groundlessness. You can’t grieve what you never had. You can’t organize around a vacancy. The affect is ambient, diffuse, hard to locate:

- Renting: the space is never quite yours to modify, inhabit fully, commit to

- Streaming: no record collection, no artifact that says “this is who I am over time”

- Gig work: no career narrative, no institutional identity, no “I work at ___”

- No project: energy with no vessel — competence that doesn’t compound into anything

The problem with living perpetually provisional: when everything is contingent, nothing accumulates. The future doesn’t build on the present in any material way and that leaves a kind of temporal flattening. One’s present doesn’t feel like it’s going anywhere, because structurally, it isn’t.

This is distinct from poverty; poverty is deprivation. Ownless is a specific modern condition where someone can be functionally comfortable — enough to eat, phone works, Netflix runs — while having zero structural stake in anything. The comfort level is high enough to prevent the desperation that produces action, but the groundlessness is deep enough to prevent the investment that produces meaning.

The trap’s design is this: “just comfortable enough not to revolt, not rooted enough to build”

What the design exploits is that ‘having your own’ thing isn’t just about income. It’s a vessel for identity; what you are is what you’re building. It’s A time horizon; you’re working toward something that doesn’t exist yet. It’s Skin in the game; the outcome matters personally, not just financially. There’s craft transmission; you develop mastery through the project’s resistance

So the ownless of today aren’t listless because they’re incurious or lazy. They’re listless because they can see the structure and can’t pull the lever. The intelligence (a college degree) that was supposed to be the ticket becomes the instrument of a very clear-eyed, very helpless understanding of the trap.

——

I started this morning asking whether now was good timing to buy a house. Rates, timing, market conditions— a 30-year-old wondering whether they can get a foothold somewhere; but I ended up somewhere else.

A house is one of the last legible accumulation mechanisms left, though a foot in the door is no easy step.

But a mortgage builds equity and the payments convert into stake over time. It is, in the most literal sense, the last and opposite state to the ownless — perhaps in the future the thing that can be most yours, that builds, that doesn’t evaporate when the subscription lapses.

The kids of the ownless tomorrow will grow up in rented homes with tools they license and careers someone platforms. What shapes the ownless won’t be deprivation; they’ll always have just enough. It will be the absence of the thing I’m still trying to figure out how to afford: something that is theirs. Something that compounds, something we can point to and say I built that, and it’s still here. Like the houses our ancestors built and imagined passing down.

That’s why the question of whether to buy a house stopped being a financial question about halfway through the research and became a question about whether the exit is still open.

I think so.